Pool Service Industry Fragmentation: Why No Company Owns More Than 10%

The pool service industry is one of the most fragmented sectors in home services. Despite a $62 billion total market, even the largest national players—Pool Corporation and Leslie's—hold less than 10% market share in their respective categories. The industry remains dominated by approximately 125,000 small, family-owned businesses.

Key Statistics

The Scale of Fragmentation

Pool Corporation, the industry's largest wholesale distributor, serves approximately 125,000 professional customers—the vast majority being small, family-owned independent contractors.[1]Pool Corporation 10-KFiscal year ended December 31, 2024SEC Filing

Most of these businesses operate with no more than 10 employees; many are "one-man-and-a-truck" operations. This structure has remained remarkably stable even as the industry has grown.

Sources: Pool Corp 10-K, Leslie's 10-K

Market Share Reality

Even the industry giants command surprisingly modest market shares. Pool Corporation reported $5.3 billion in 2024 net sales within a total industry valued at $62 billion by the Pool & Hot Tub Alliance—representing just 8.5% of the total market.[3]Pool Corp Q4 2025 Earnings CallFebruary 2026Transcript[4]PHTA Industry Revenue Report2025 Press ReleasePHTA Website

| Company | Revenue | Market | Share |

|---|---|---|---|

| Pool Corporation | $5.3B | $62B Total Industry | 8.5% |

| Leslie's | $1.45B | $15B Care Aftermarket | 9.7% |

The chart below visualizes this market share reality—even the largest players command less than 10% of their respective markets, leaving the vast majority of industry activity distributed among thousands of smaller operators.

The Independent Advantage

Leslie's operates 1,021 branded retail locations—making it the largest national specialty pool care retailer.[2]Leslie's, Inc. 10-KFiscal year ended September 28, 2024SEC Filing Yet independent retailers still outnumber Leslie's stores by nearly 8 to 1.

This means there are approximately 7.8 independent pool retail locations for every 1 Leslie's store—a ratio that has remained relatively stable over the past decade.

Key Insight

The pool industry remains one of the most fragmented in home services. While the largest national distributor and retailer have achieved roughly 8.5% to 10% market share in their respective categories, the labor-heavy service sector is dominated by 125,000 mostly family-owned small firms—many with fewer than 10 employees.

Why Fragmentation Persists

Several structural factors explain why the pool service industry has resisted consolidation:

1. Local Relationship Model

Pool service is inherently local. Customers prefer dealing with technicians they know and trust, who understand their specific pool and equipment. This relationship-driven model makes it difficult for national chains to replicate the service quality of established local operators.

2. Low Barriers to Entry

Starting a pool service business requires relatively modest capital investment—often just a truck, basic equipment, and chemicals. The low startup costs enable constant new market entry, maintaining competitive pressure.

3. Route Economics

Pool routes have natural geographic boundaries based on drive time efficiency. A single technician can typically service 12-18 pools per day within a tight geographic area. Expansion beyond these boundaries requires adding trucks and technicians, which replicates the small-business model rather than achieving economies of scale.

4. Labor Intensity

Unlike product distribution (Pool Corp) or retail (Leslie's), pool service cannot be easily automated or centralized. Each pool requires physical on-site work, limiting the scalability advantages that drive consolidation in other industries.

The Consolidation Pressures Pros Feel

While the numbers show fragmentation persists, the forces pushing against it are real. Pool pros feel them every week.

Private Equity Rollups

Private equity firms are actively buying pool service companies. Many owners report getting two or three cold calls per week from buyers looking to acquire routes and accounts. These PE-backed companies have large marketing budgets that drive up the cost of Google and Facebook ads for everyone.

"Every week, two or three cold calls hit my desk: 'We'd love to buy your business.' These firms have bottomless ad budgets and are blowing out the cost of online marketing. Competing with someone spending $30,000 a month on PPC isn't a game of grit. It's a rigged match."

— Pool pro via Reddit

The rollups create a two-tier market. PE-backed companies can outspend independents on advertising while operating at lower margins because they are optimizing for growth, not profit. For the independent owner, this means higher customer acquisition costs without any change in what they can charge.

Distributors Competing With Their Customers

The distributor relationship has grown more complicated. Pool Corporation owns both Heritage and SCP, the two largest equipment distributors. Through its Pinch A Penny franchise network, the company also operates retail locations that compete directly with the same service professionals it supplies.

"SCP has entered the residential market directly through their Pinch A Penny franchises. While smiling at us across the counter, they're now setting up shop across the street."

— Pool pro via Reddit

At the same time, Amazon and online gray-market sellers have made pool equipment available to homeowners at prices that sometimes undercut wholesale. Pros find themselves competing with their own supply chain.

Leslie's faces its own challenges. The chain's stock has dropped sharply, and pros who use their stores as distributors worry about losing access to local inventory. Some stores offer trade pricing competitive with SCP and Superior, while others push retail products on homeowners that contradict what the service pro recommends.

"I use two of their stores as distributors. The trade pricing is same as Superior and the staff are good guys. Their corporate is a bunch of shitheels that won't put money where it's needed. Support pros? Nah, push Perfect Weekly on retirees."

— Pool pro via Reddit

"My local Leslie's tells my clients the wildest shit. It's like they see what's trending on TikTok and tell people to do that."

— Pool pro via Reddit

The tension is clear: pros depend on local stores for same-day parts, but corporate retail chains often undermine the service relationship by giving homeowners conflicting advice. Independent pool supply shops avoid this conflict, which is why many pros prefer them despite fewer locations.

Manufacturer Loyalty Cuts Both Ways

Even long-standing distributor relationships are not safe. One distributor with over 40 years of Pentair purchasing was cut off with just weeks of notice after Pentair set a $300,000 per year minimum threshold.

"Wanna know what Pentair did to us mid-December 2024? They cut us off. Customer of over 40 years, straight up said as of January 1 we cannot buy from them anymore. They set a threshold of $300K per year to continue as a distributor."

— Pool equipment distributor via Reddit

These dynamics explain why fragmentation persists even as large players push to consolidate. The independent advantage is real, but it requires constant adaptation. Pros who diversify their supply chain, build strong local relationships, and invest in efficiency tools are the ones who survive the squeeze. For more on handling rising costs, see our guide to pool equipment price increases in 2026.

Wholesale Support Density

Pool Corporation operates 456 sales centers across the country, serving those 125,000 professional customers. This translates to approximately 274 service/retail businesses per wholesale location.[3]Pool Corp Q4 2025 Earnings CallFebruary 2026Transcript

| Metric | Value | Calculation |

|---|---|---|

| Professional Customers | 125,000 | Pool Corp wholesale customers |

| Sales Centers | 456 | Pool Corp domestic locations |

| Businesses per Center | 274 | 125,000 ÷ 456 |

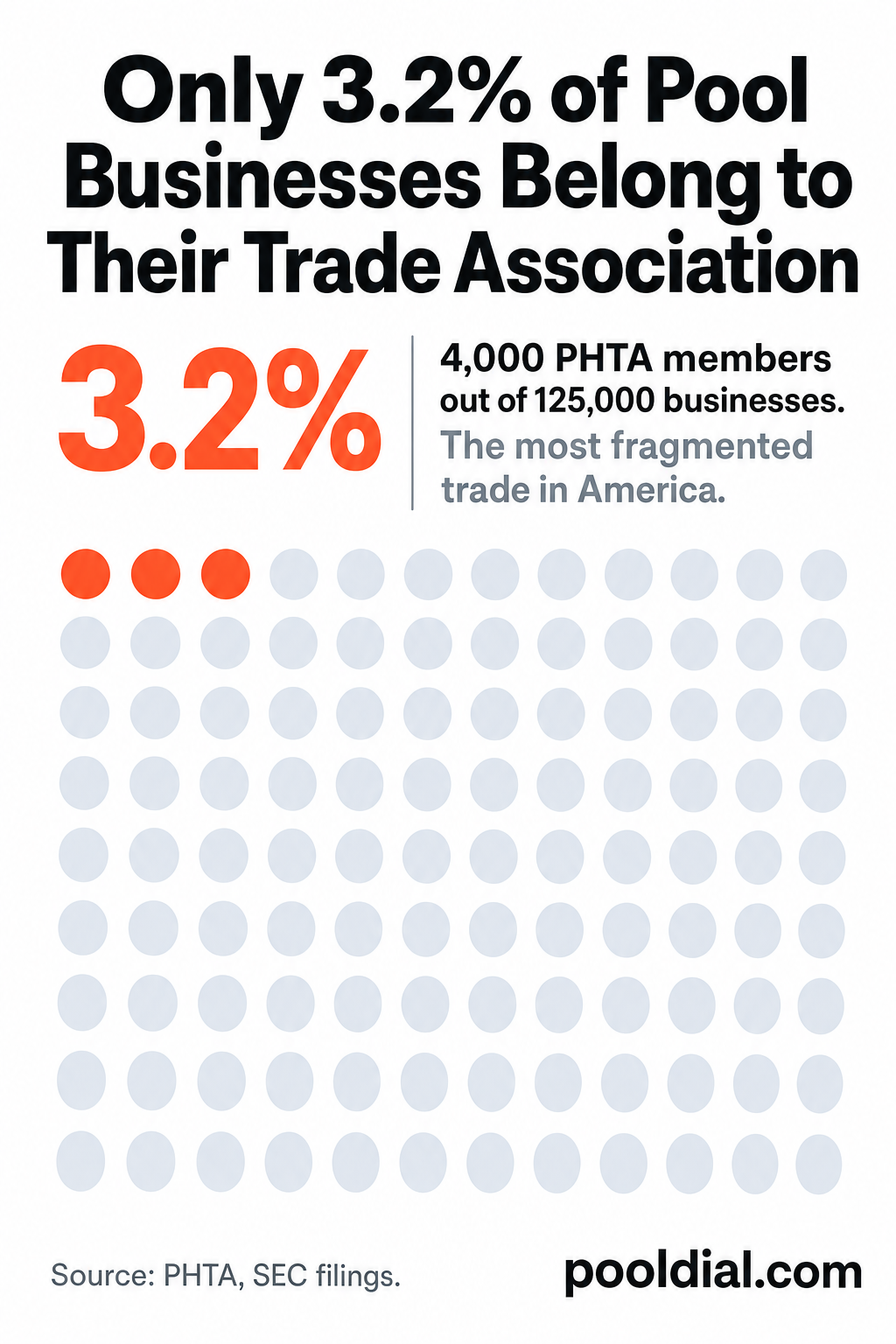

PHTA Membership Context

The Pool & Hot Tub Alliance reports approximately 4,000 member organizations worldwide.[4]PHTA Industry Revenue Report2025 Press ReleasePHTA Website This represents just 3.2% of the estimated 125,000 professional businesses—suggesting the vast majority of pool service operators remain unaffiliated with the industry's primary trade association.

What This Means for Pool Service Businesses

The fragmented market structure creates both challenges and opportunities:

- Opportunity: Small operators can compete effectively against national players through superior local service and relationships

- Challenge: Limited buying power compared to larger competitors—though chemical pricing strategies can help

- Opportunity: Technology can help small operators achieve efficiency gains without losing their local advantage

- Challenge: Recruiting and retention remain difficult when competing with larger employers for talent

For more industry data, see our analysis of how many pool service companies are in the US and the pool industry statistics for 2026.

Compete Smarter in a Fragmented Market

PoolDial helps small pool service businesses operate with the efficiency of larger competitors—route optimization, automated billing, and customer management in one platform.

Start Your Free TrialSources

- [1] Pool Corporation Annual Report (Form 10-K) — Fiscal year ended December 31, 2024. SEC Filing

- [2] Leslie's, Inc. Annual Report (Form 10-K) — Fiscal year ended September 28, 2024. SEC Filing

- [3] Pool Corporation Q4 2025 Earnings Call — February 2026. Transcript

- [4] Pool & Hot Tub Alliance — Industry Revenue Holds Steady Despite Profit Margin Pressure, 2025. PHTA Press Release